Should I Wait for Mortgage Rates to Hit 5.9% or Buy at 6.3% Now?

Should you wait for mortgage rates to drop to 5.9% or buy now at 6.3%? Here is the real math, the local data, and the rate optimization strategies most buyers don't know about.

Should I Wait for Mortgage Rates to Drop to 5.9%, or Buy Now at 6.3%?

Should I wait for mortgage rates to drop to 5.9%, or buy now at 6.3%?

On a $450,000 loan, the difference between 6.3% and 5.9% is $116 per month — $1,395 per year, or $41,855 over the life of a 30-year mortgage. That savings is real, but it only materializes if rates actually reach 5.9% and if the home you want hasn't changed in price or negotiating terms by the time they do. In today's Southwest Valley market, where prices per square foot in the $400K–$500K range are down 3.6% year-over-year and sellers are contributing to buydowns, buying now with a rate optimization strategy may put you in a stronger position than waiting for a number that isn't guaranteed.

What This Question Is Really About

If you are asking this question, the rate is rarely the actual concern underneath it. The real question is closer to: "What if I buy now and regret it six months later when rates are lower?" That fear of making the wrong call at the wrong time is legitimate — and it's the single most common reason buyers in the $400K–$600K range stay on the sidelines longer than they need to.

Here's what I want you to hold alongside that concern: timing the rate is only one variable in a decision that involves price, inventory, seller motivation, and your personal timeline. The buyers who tend to do well in markets like this are the ones who optimize across all of those variables — not the ones who wait for a single number to land.

The data right now tells a more nuanced story than most buyers realize, and it's worth slowing down to look at it clearly before making a decision in either direction.

What the Rate Difference Actually Costs You

Let's start with the math, because it's often misunderstood.

On a $450,000 loan, the monthly payment at 6.3% is $2,785. At 5.9%, it's $2,669. The difference is $116 per month — $1,395 per year, or $41,855 over the full 30-year term. That's real money. I'm not going to minimize it.

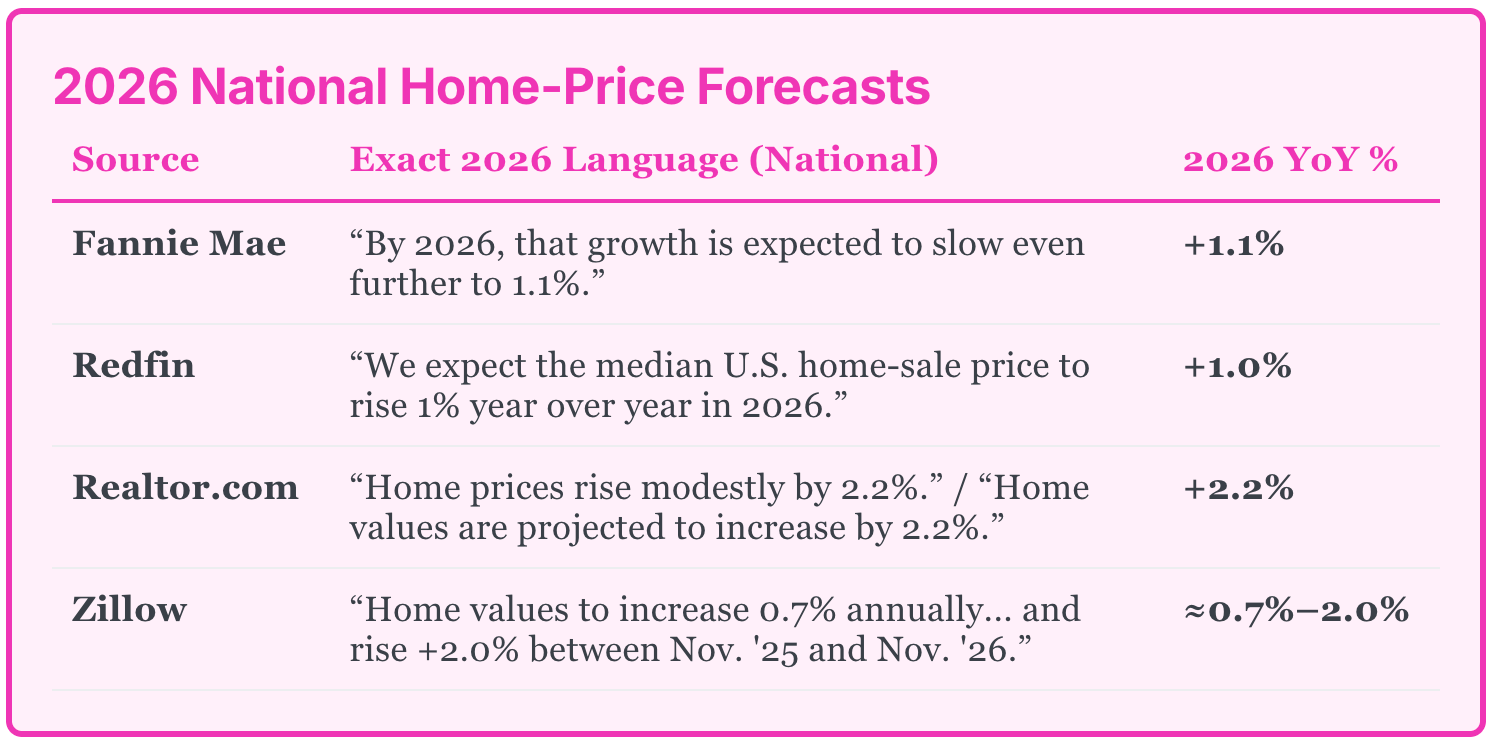

But what I want you to hold alongside that number is this: national forecasts from Fannie Mae (+1.1%), Redfin (+1.0%), Realtor.com (+2.2%), and Zillow (+0.7%–2.0%) are projecting modest home price growth in 2026. Those are U.S. averages with no clean Phoenix-specific figure. The local data tells a different story — and that's what matters for your decision.

What's Actually Happening in the West Valley Right Now

This is where it gets interesting for buyers in our market.

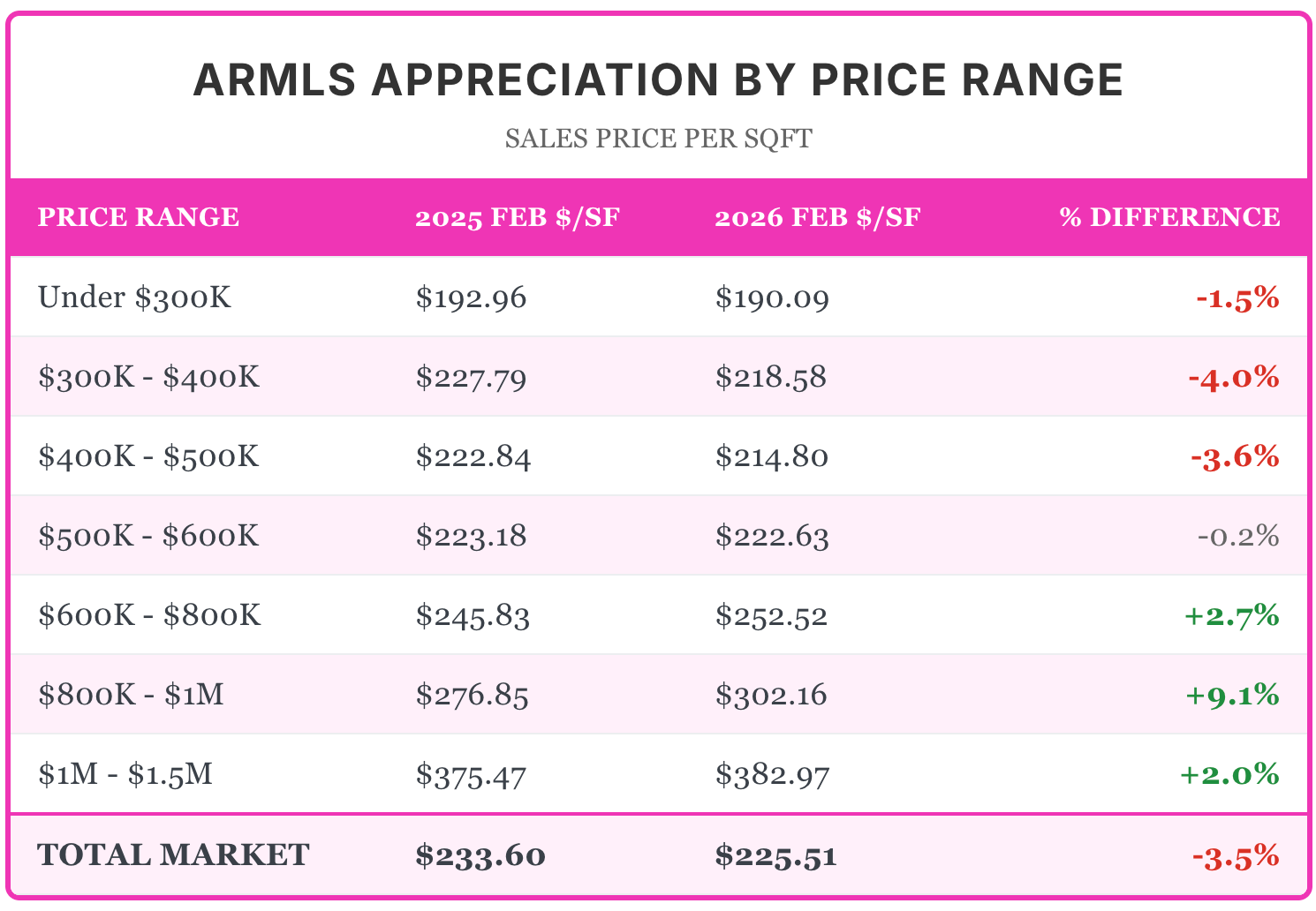

According to ARMLS data for Southwest Valley cities in February 2026, prices per square foot in the $400K–$500K range are down 3.6% year-over-year — from $222.84 to $214.80 per square foot. In the $500K–$600K range, they're essentially flat at -0.2%. The $600K–$800K range is appreciating at +2.7%, and the $800K–$1M segment is up 9.1%. The softening is concentrated in the price range where most first-time and move-up buyers are actively looking. That's a buyer-friendly environment — one that gives you negotiating room that didn't exist 18 months ago.

What I watch for when this kind of data comes in: a softening in the entry-level and mid-range doesn't usually last forever in a market with the structural demand Phoenix has. When rates do move lower, buyers who've been sitting on the sidelines re-enter simultaneously — and that negotiating room tends to narrow fast. The buyers who do well in a market like this are the ones who move during the soft patch, not after it.

Homes are selling. The difference is they're selling at terms that favor buyers — and that's a window worth paying attention to.

The Strategy I'd Walk You Through: The 2–1 Buydown

This is usually where I slow buyers down, because most people haven't heard of this option and it changes the math significantly.

A 2–1 buydown lets you purchase at today's softened price while reducing your effective interest rate for the first two years. On a $450,000 loan at a base rate of 6.3%, the structure looks like this: your first year rate drops to 4.3%, bringing the monthly payment to $2,227 — that's $558 less per month than the full rate. In year two, the rate steps up to 5.3% at $2,499 per month, saving you $287 monthly. From year three forward, you're at the full 6.3% rate of $2,785. The total two-year savings comes to approximately $10,140.

Your year-one rate of 4.3% is better than the 5.9% you're waiting for. And in the current market, asking the seller to contribute toward the buydown cost is a reasonable negotiation — not an unusual request. I've helped clients structure this successfully where the seller covers half and the buyer covers half. You pay $5,000; they cover $5,000. Everyone moves forward.

If rates do drop to 5.9% or lower during that two-year window, you explore a refinance from a position of ownership — not from the sidelines. Bankrate's guide to mortgage points and buydown structures is a good reference if you want to go deeper on how these are calculated. And if a refinance ever makes sense, know that it typically costs 2–6% of the loan amount — so factor that into any future decision. Bankrate's refinancing cost breakdown walks through the full picture.

The 2–1 Buydown Isn't the Only Option

The temporary buydown gets the most attention, but it's not the only way to get your effective rate closer to — or even below — the 5.9% you're waiting for.

Permanent rate buydowns are another tool worth understanding. Instead of a temporary reduction that resets after two years, you pay discount points upfront to permanently lower your rate for the life of the loan. One point (1% of the loan amount, or $4,500 on a $450,000 loan) typically reduces your rate by roughly 0.25%. So buying two points at a cost of $9,000 could bring a 6.3% rate down to approximately 5.8% — permanently. That's not a two-year window; that's your rate for the full 30 years or until you refinance. The math on points works best when you plan to stay in the home for at least four to five years, which is where the break-even point typically falls.

New construction incentives are the piece of this equation that surprises most buyers right now. Builders across the West Valley — particularly those with standing inventory or quick move-in homes — are actively competing for buyers through their preferred lender programs. What I'm seeing with clients is builder incentives that include rate buydowns (both temporary and permanent), closing cost credits, and in some cases below-market rates through the builder's affiliated lender. These incentives can stack. A builder offering a permanent buydown to 5.5% or 5.75% through their preferred lender, combined with $10,000–$15,000 in closing cost credits, can put your effective rate and out-of-pocket costs well below what you'd achieve waiting for rates to drop on their own. The trade-off is that using the builder's preferred lender sometimes means less flexibility on loan terms — so you want to compare the full picture, not just the rate.

Here's how I frame this for buyers: the 2–1 buydown, permanent points, and new build incentives are three different paths to the same destination — a lower effective rate today. Which one makes sense depends on whether you're buying resale or new construction, how long you plan to hold the home, and how much cash you want to deploy upfront versus saving for reserves. This is exactly the kind of conversation I walk clients through before they commit to a strategy.

— Mariah A, Phoenix, AZ

Three Ways to Think About This Decision

At this stage, I help clients narrow their focus to which strategy actually fits their situation — not which one sounds best in theory.

Buy now and optimize the rate. Whether through a 2–1 buydown, permanent discount points, or new build incentives, you own the home at today's softened prices with an effective rate that can match or beat the 5.9% you're waiting for. You build equity from day one. If rates improve further, you refinance. This is the approach I'd walk most buyers through in the current market — not because it's perfect, but because it doesn't require you to predict the future correctly.

Wait for 5.9%. The savings are real if everything goes as planned. But here's what I want you to think through: when rates drop, other buyers re-enter the market at the same moment. The sellers who are currently contributing to buydowns and accepting below-list offers become less motivated to do so. The soft patch you're navigating right now may not be the market you're buying into at 5.9%. You could save $116 per month and lose $10,000–$15,000 in negotiating position. That math doesn't always work in the waiting buyer's favor.

Set a trigger and a deadline. If you have genuine flexibility — your lease isn't ending, no relocation pressure — set a specific trigger: "If rates hit 5.9% by [date], I'll buy then." But also set a price ceiling: "If the home I want has appreciated meaningfully by then, I'm buying regardless of rate." Don't let one variable drive a decision that involves several. And don't let an open-ended wait become indefinite delay.

If you're also managing the timing of a current home sale, our guide on contingent offers and rent-backs in Goodyear walks through how to structure that transition without creating unnecessary pressure on either side.

Why the Long-Term Case for West Valley Ownership Is Unusually Strong

I want to zoom out for a moment, because this is the part of the conversation I think matters most — and it rarely gets enough attention when buyers are focused on rate movements.

The Arizona Office of Economic Opportunity's December 2025 projections show Maricopa County growing from 4.79 million people today to 6.07 million by 2060 — 1.28 million additional residents, a 27% increase. By 2060, Metro Phoenix will represent 73.5% of Arizona's entire population. The Maricopa Association of Governments projects the Phoenix MSA's job base to roughly double over the same period.

The West Valley is the primary corridor for that expansion. Developers aren't speculating on this — they're buying land and building infrastructure with 10–30 year horizons. Economic development continues to generate jobs in logistics, semiconductor manufacturing, healthcare, and distribution, much of it concentrated along the freeway corridors that run directly through our market.

Near-term headwinds are real. Rising costs, geopolitical uncertainty, and economic caution affect buyer sentiment and can create short-term pauses in demand. I'm not going to pretend otherwise. But these factors don't reverse migration patterns that have been building for decades, and they don't cancel the infrastructure already under construction. The structural case for West Valley real estate is built on 35 years of projected growth — not on a favorable quarter. For buyers thinking of this purchase as a stepping stone — building equity while your family's needs evolve — the long-term demand trajectory is the foundation that makes the strategy work.

— S B, Tempe, AZ

One More Number I Think Every Buyer Should Know

According to the Federal Reserve Board Survey of Consumer Finances, the median homeowner net worth in 2022 was approximately $396,000 — 38 times the median renter net worth of roughly $10,400. This ratio has held across every measured period since 1989. It's not primarily about appreciation. It's about the forced savings mechanism of a mortgage, the leverage of owning an asset, and the compounding effect of equity over time.

The $116 per month rate savings you might capture at 5.9% doesn't close a 38x net worth gap. Getting into ownership does.

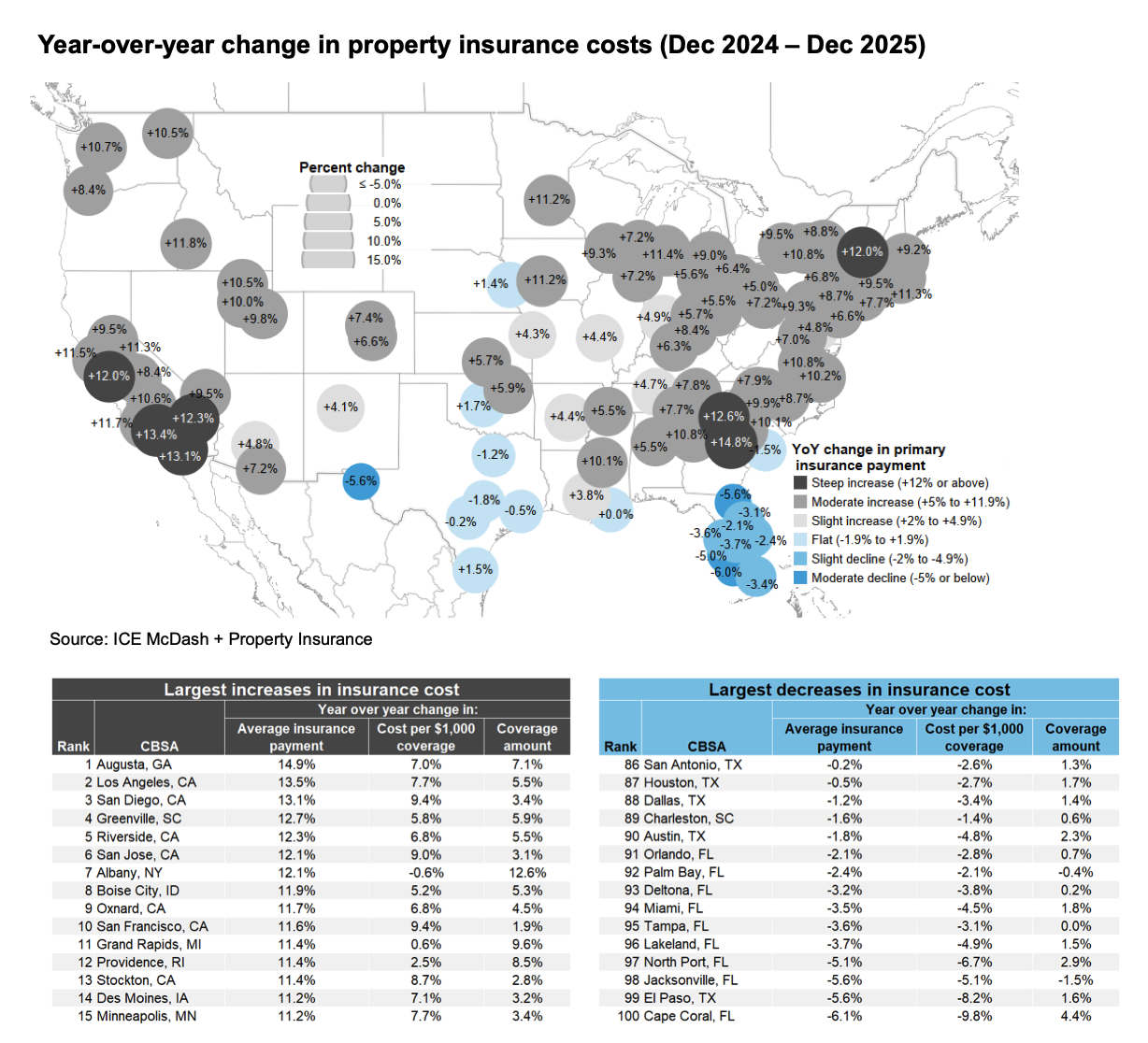

And while we're talking about carrying costs: Phoenix metro property insurance increased approximately 4.8% year-over-year between December 2024 and December 2025, according to ICE McDash data. That's moderate compared to California markets like Los Angeles (+13.5%) and San Diego (+13.1%), and far more stable than Florida metros where costs are actually declining after years of sharp increases. Insurance is a real and rising cost — but as an owner, your principal and interest payment is fixed. As a renter, every rising cost a landlord faces eventually finds its way into your rent.

FAQ: Waiting for Rates vs. Buying Now in the West Valley

Q: What's the real monthly payment difference between 6.3% and 5.9%?

A: On a $450,000 loan, it's $116 per month — $1,395 per year, or $41,855 over 30 years. That's real money. But it only materializes if rates reach 5.9% and the home you want hasn't changed in price or negotiating terms by then.

Q: Are West Valley home prices going up or down right now?

A: In the $400K–$500K range, Southwest Valley prices per square foot are down 3.6% year-over-year as of February 2026, according to ARMLS data. In the $500K–$600K range, they're essentially flat at -0.2%. For buyers in this range, this is one of the more favorable entry points in several years.

Q: What is a 2–1 buydown and what does it actually save me?

A: On a $450,000 loan at 6.3%, a 2–1 buydown gives you 4.3% in year one ($2,227 per month) and 5.3% in year two ($2,499 per month), then 6.3% from year three onward. Total two-year savings: approximately $10,140. Asking the seller to contribute is a reasonable negotiation in this market. Bankrate's mortgage points guide walks through the full breakdown.

Q: Can I get a rate below 5.9% right now without waiting?

A: Yes. A 2–1 buydown gives you 4.3% in year one. Permanent discount points can bring your rate to approximately 5.8% for the life of the loan. And new construction builders across the West Valley are offering preferred lender incentives that can include below-market rates in the 5.5%–5.75% range combined with closing cost credits. Each option involves different trade-offs — the right one depends on whether you're buying resale or new, how long you plan to stay, and your cash reserves.

Q: What do the national forecasts say about 2026 home prices?

A: Fannie Mae (+1.1%), Redfin (+1.0%), Realtor.com (+2.2%), and Zillow (+0.7%–2.0%) are all projecting modest national appreciation — but these are U.S. averages. The Southwest Valley ARMLS data is the more relevant benchmark for buyers in our market.

Q: Why does long-term population growth matter to my buying decision today?

A: Because demand for housing in this region is structural, not cyclical. Maricopa County is projected to add 1.28 million residents by 2060, according to the Arizona Office of Economic Opportunity. The Phoenix MSA job base is projected to roughly double. The West Valley sits directly in that growth corridor. You're not just buying a home — you're positioning yourself in one of the fastest-growing regions in the country.

Q: What if I wait and rates don't drop?

A: Then you've waited, prices have likely stabilized or risen, and you're buying into a market where sellers have less motivation to contribute to buydowns or negotiate on price. Set a specific rate trigger and a deadline. If rates don't cooperate by then, commit. Don't let the open-ended wait become the default strategy.

The Bottom Line

Here's where I land after working through this with buyers across the West Valley: if you've found the right home in the right neighborhood at the right price for your life, the rate is one variable — not the whole decision.

Rates can be optimized through buydowns, negotiation, and future refinancing. The neighborhood, the community, the school zone, the commute — those are foundational. And right now, in the $400K–$600K range across the Southwest Valley, prices have softened and sellers are negotiating. That's a window. It won't stay open indefinitely.

Whether you are buying, selling, or relocating, if you're looking for guidance and a personalized approach, we are here to help you make moves with strategy, clarity, and confidence.

Let's Chat!

📞 928-910-7401

📧 home@chavezdreamhometeam.com

🌐 chavezdreamhometeam.com

And if you're searching in the sub-$450K range in the West Valley, our guide to homes under $400K in the West Valley breaks down where real opportunities still exist without settling for a fixer-upper.

About the Author

Kasandra Chavez is a real estate advisor serving the West Valley of Greater Phoenix, Arizona, recognized among the top 5% of real estate professionals in the Greater Phoenix area. She partners with buyers and sellers to develop strategies aligned with their lifestyle, financial goals, and timeline — helping them make confident, well-informed decisions. Her approach is grounded in market data, process transparency, and steady advocacy from first conversation through closing.